Why Subchapter V Plans Are Approved Faster Than Traditional Chapter 11 Plans

- Melissa A. Youngman

- Mar 3

- 10 min read

By Melissa A. Youngman Florida Chapter 11 & Subchapter V Business Reorganization Attorney | Winter Park, FL

When a business is in financial distress, time is not a luxury. Every week spent in an extended bankruptcy process is a week of uncertainty for employees, customers, vendors, and the business owner trying to hold everything together.

This is one of the most important practical differences between Subchapter V and traditional Chapter 11: Subchapter V plans are confirmed significantly faster, and the reasons why are built directly into the structure of the law.

For small and mid-sized business owners in Winter Park, Orlando, Maitland, Altamonte Springs, Kissimmee, and throughout Central Florida, understanding why Subchapter V moves faster, and what that means for your business, can make the difference between choosing the right restructuring path and spending more time and money than necessary.

This post breaks down exactly where Subchapter V eliminates the bottlenecks that slow traditional Chapter 11 cases to a crawl.

The Traditional Chapter 11 Timeline Problem

To understand why Subchapter V is faster, it helps to understand why traditional Chapter 11 is slow.

A conventional Chapter 11 case involves multiple layers of procedural requirements, each designed for large, complex corporate reorganizations. When applied to a small or mid-sized business, those same procedures don't become simpler. They remain just as burdensome, just as expensive, and just as time-consuming.

The result: many small businesses that entered traditional Chapter 11 with a viable reorganization plan ran out of time, money, or both before ever reaching confirmation. Congress recognized this problem and created Subchapter V through the Small Business Reorganization Act of 2019 specifically to fix it. Here is where the time savings actually come from.

Reason 1: No Disclosure Statement Required

In a traditional Chapter 11 case, before a business can even begin soliciting creditor votes on its reorganization plan, it must first prepare and file a detailed Disclosure Statement.

The Disclosure Statement is a comprehensive document that typically includes the full history of the business, a complete description of assets and liabilities, financial projections, an analysis of what creditors would receive in a Chapter 7 liquidation, and a thorough explanation of how the plan will be funded. It can run dozens of pages or more.

Once filed, the Disclosure Statement must be approved by the bankruptcy court before the debtor can send it to creditors. That approval process involves a hearing (and often rounds of objections and revisions) before the court signs off. Only then can the solicitation and creditor voting process begin.

In Subchapter V, there is no Disclosure Statement requirement.

Instead, the plan itself must include certain key disclosures: a brief history of the business, a liquidation analysis, and projections showing the debtor's ability to make plan payments. This is far less extensive than a full Disclosure Statement, and it does not require a separate court approval hearing before the plan can move forward. Eliminating the Disclosure Statement process alone removes weeks, sometimes months, from the timeline.

Reason 2: No Creditor Committee to Negotiate With

In traditional large Chapter 11 cases, an Official Committee of Unsecured Creditors is typically formed to represent the interests of all unsecured creditors. The committee hires its own attorneys and financial advisors, and the debtor's estate pays those professional fees.

The creditor committee reviews the debtor's finances, investigates the business, and negotiates the terms of the reorganization plan. That process adds significant time and expense to a case. Committee professionals file their own motions, conduct their own discovery, and must approve or object to major decisions throughout the proceeding.

For small businesses, this dynamic is particularly problematic. Individual creditor claims may be too small to justify the committee's participation from a pure cost-benefit standpoint, yet the committee process moves forward regardless.

In Subchapter V, there is no mandatory creditor committee.

A committee can be appointed by the court for cause, but in the vast majority of Subchapter V cases, none is formed. This eliminates an entire layer of negotiation, professional fee generation, and procedural delay that is baked into traditional Chapter 11.

Without a committee, the debtor works directly with the Subchapter V trustee, whose role is to facilitate a consensual plan, not to adversarially represent creditor interests. That is a fundamentally different dynamic, and it moves cases forward faster.

Reason 3: The Plan Filing Deadline Is 90 Days

In a traditional Chapter 11 case, the debtor has an exclusivity period of 120 days to file a plan of reorganization. If the debtor does not file within that window and the court extends it, the exclusivity period can stretch to 18 months during which no plan may be confirmed and the clock keeps running on administrative costs.

Even in a "small business" Chapter 11 (a separate designation under the Bankruptcy Code), the deadline to file a plan is 300 days from the petition date. That is nearly a year of case administration before a plan is even on file.

In Subchapter V, the debtor must file a plan within 90 days of the petition date.

That 90-day deadline is not merely aspirational. It is a structural requirement built into the law. The court can extend it for cause, but the default expectation is that the plan will be on file within three months of filing, and the case will proceed to confirmation shortly thereafter.

This compressed timeline has a powerful practical effect: it forces early focus on the reorganization strategy and reduces the period during which the business is operating under the uncertainty and cost of an open bankruptcy case.

Reason 4: The Plan Can Be Confirmed Without a Single Creditor Vote

This is one of the most significant (and most misunderstood) features of Subchapter V.

In traditional Chapter 11, plan confirmation requires at least one class of impaired creditors to vote in favor of the plan. If creditors refuse to vote, or vote against the plan, the debtor faces a difficult and expensive "cram-down" process that requires satisfying additional legal standards, including the absolute priority rule, which generally prohibits business owners from retaining any equity interest unless all creditors are paid in full.

Getting creditor acceptance in a traditional Chapter 11 can be an extended and contentious process. Creditors who disagree with the plan's terms have significant leverage. Negotiations stall. Hearings are scheduled and rescheduled. The case drags on.

In Subchapter V, a plan can be confirmed by the court even if no creditor votes in favor of it. The court evaluates the plan for fairness, feasibility, and equitable treatment of creditors. If the plan meets the statutory requirements, including providing creditors with at least as much as they would receive in a Chapter 7 liquidation and committing the debtor's projected disposable income to plan payments over three to five years, the court can confirm the debtor's plan without creditor approval.

This feature does not mean creditors have no rights in Subchapter V. Creditors retain meaningful protections. But the removal of the minimum creditor vote requirement as a condition of confirmation eliminates one of the primary bottlenecks in traditional Chapter 11, and removes the leverage creditors previously used to extract plan concessions that prolonged or derailed reorganizations.

Reason 5: The Absolute Priority Rule Does Not Apply

In a traditional Chapter 11, the absolute priority rule dictates that a business owner cannot retain any equity interest in the reorganized company unless all senior creditors are paid in full. This rule creates enormous complexity in plan negotiations. Creditors know that the owner's desire to retain the business gives them leverage. Protracted negotiations over the value of the business, and what the owner must pay to retain it, are among the most time-consuming features of traditional Chapter 11 cases.

Subchapter V eliminates the absolute priority rule entirely.

Business owners in Subchapter V can retain their equity interest in the reorganized company even when unsecured creditors are not paid in full, provided the plan commits the debtor's projected disposable income to creditor payments for the plan term. This fundamental change removes one of the most contentious points of negotiation in plan confirmation, and with it, a significant source of delay.

Reason 6: Only the Debtor Can Propose a Plan

In traditional Chapter 11, the debtor has an initial exclusivity period during which it alone can file a plan. But if that period expires without a confirmed plan, which happens frequently, creditors, creditor committees, or other parties in interest can file their own competing plan.

Competing plans create complexity. The court must evaluate multiple proposals. Competing parties conduct discovery and file motions. The confirmation process expands in scope and duration.

In Subchapter V, only the debtor may file a plan at any point in the case.

Creditors have no right to propose a competing plan in Subchapter V, regardless of how long the case has been pending. This keeps the reorganization process focused on the debtor's proposal, reduces procedural complexity, and eliminates the possibility of a creditor-driven plan that the business owner had no hand in drafting.

Reason 7: No Quarterly U.S. Trustee Fees

In traditional Chapter 11 cases, the debtor must pay quarterly fees to the U.S. Trustee's office based on the amount of disbursements made during the case. These fees can be substantial, and they accumulate throughout the life of the case, which means the longer the case runs, the more fees accrue.

Subchapter V debtors are expressly exempt from quarterly U.S. Trustee fees.

This is not directly a time-savings measure. However, for small businesses, eliminating this ongoing cost removes pressure that might otherwise force premature decisions.

What This Means for Central Florida Business Owners

The practical effect of these seven differences is a Subchapter V case that typically moves from filing to plan confirmation in three to five months compared to traditional Chapter 11 cases that routinely take one to two years or more before a plan is confirmed.

For a restaurant in Winter Park, a contractor in Longwood, a retailer in Maitland, or a hospitality business near International Drive, that difference is enormous. A confirmed plan in five months means the business has a clear path forward in the same year it filed. A case that drags for 18 months means 18 months of professional fees, operational uncertainty, and management distraction.

Speed matters. And Subchapter V is built to be fast.

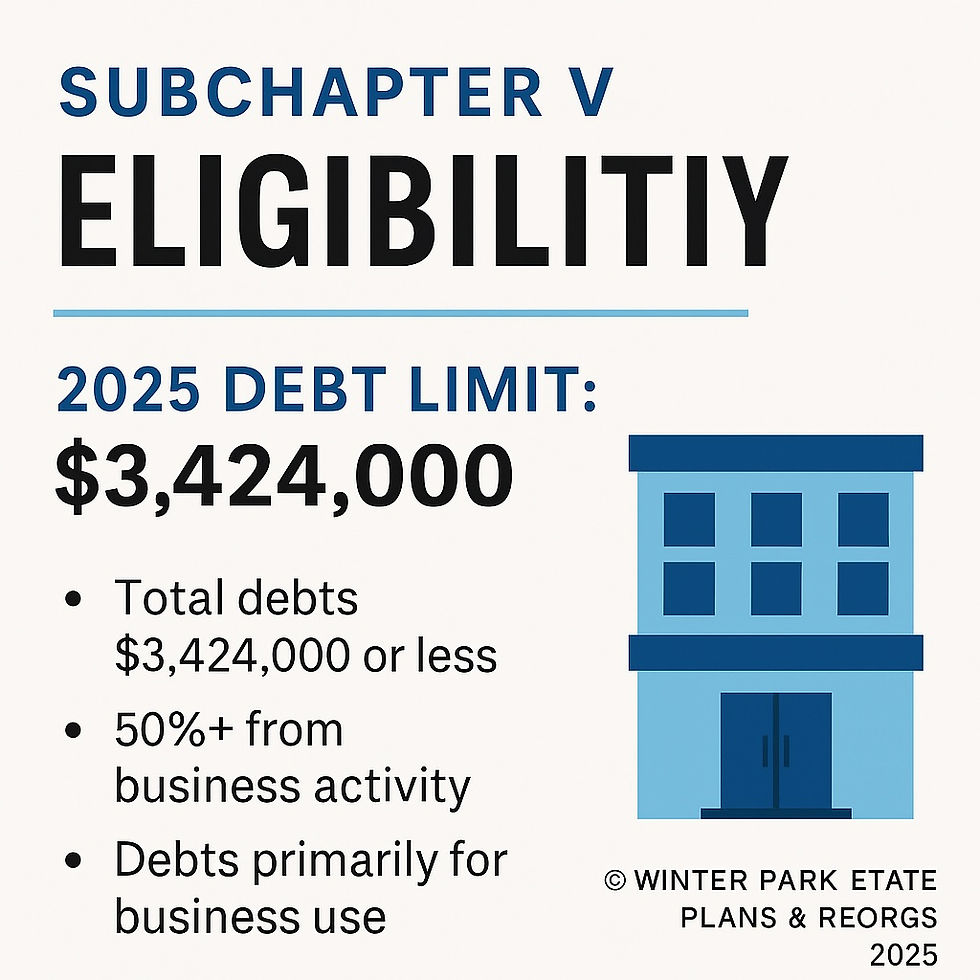

Is Your Business Eligible for Subchapter V?

Not every business qualifies for Subchapter V. To be eligible, a debtor must:

Be engaged in commercial or business activities (single-asset real estate operations generally do not qualify)

Have total non-contingent, liquidated secured and unsecured debts at or below the current statutory threshold (currently $3,424,000 as of the most recent adjustment — consult an attorney for the most current figure)

Have at least 50% of those debts arise from business activities

If your business debt exceeds the current threshold, traditional Chapter 11, including a standard small business case, may be the appropriate path. An experienced bankruptcy attorney can help you calculate eligibility accurately, including which debts count toward the cap and how to structure the analysis.

Warning Signs That It May Be Time to Evaluate Subchapter V

If any of the following apply to your Central Florida business, a conversation with a reorganization attorney may be overdue:

✔ You are behind on commercial rent by more than one month

✔ A creditor has filed suit or obtained a judgment against your business

✔ You are personally liable for business debt through a personal guarantee

✔ Vendors have threatened to cut off supply or have already done so

✔ You have taken on merchant cash advances or high-interest emergency financing to cover operating expenses

✔ Your bank account has been levied or frozen

✔ You have received a Notice of Default or lease termination notice

✔ You are heading into a slow revenue period with prior debt still unresolved

The earlier a business owner explores Subchapter V, the more runway there is to use it effectively. Once critical leases terminate or judgment liens attach, certain options become unavailable or significantly more difficult to pursue.

Frequently Asked Questions

Does faster confirmation mean less protection for my business? No. The automatic stay goes into effect immediately upon filing in Subchapter V, just as it does in traditional Chapter 11. All creditor actions, including lawsuits, garnishments, evictions, and repossessions, are halted from the moment the case is filed.

Can creditors still object to a Subchapter V plan? Yes. Creditors retain meaningful rights in Subchapter V. They can object to plan confirmation on grounds including feasibility, fairness, and whether they are receiving at least as much as they would in a Chapter 7 liquidation. The difference is that their vote is not required. The court makes the determination.

What happens if the business cannot meet plan payments after confirmation? Subchapter V includes provisions for plan modification post-confirmation. The debtor (and only the debtor) may seek to modify a confirmed plan if circumstances change. This is an important protection that traditional Chapter 11 also provides.

Does Subchapter V work for businesses with personal guarantees? Business bankruptcy generally does not discharge personal guarantees. However, Subchapter V may provide leverage for negotiation with guaranty creditors and can create a more stable business entity from which to address those obligations. This is a fact-specific analysis that should be discussed with an attorney.

Does the Subchapter V trustee take over my business? No. The Subchapter V trustee's primary role is to facilitate a consensual plan of reorganization and ensure the debtor complies with reporting requirements. You remain in control of the business as the debtor-in-possession. Unlike a Chapter 7 trustee, the Subchapter V trustee does not take over operations or liquidate assets.

Speak with a Central Florida Subchapter V Attorney

For eligible small and mid-sized businesses, Subchapter V is the most efficient reorganization tool available under the Bankruptcy Code. It is faster than traditional Chapter 11, less expensive, and structured to give business owners the best possible chance at a confirmed plan — often without creditor approval.

At Winter Park Estate Plans & ReOrgs, we work with business owners throughout Central Florida to evaluate whether Subchapter V is the right path, calculate eligibility, and develop a plan of reorganization designed to be confirmed quickly and built to succeed.

Early guidance preserves options. Waiting closes them.

📞 (407) 765-3427 ✉️ my@melissayoungman.com

👉 Schedule a confidential consultation with Melissa Youngman, your Winter Park Subchapter V attorney.

📥 Download our Chapter 11 & Subchapter V Readiness Checklist to understand what information you will need before filing.

📖 Read our full Guide to Florida Chapter 11 and Subchapter V for business owners.

This blog post is for informational purposes only and does not constitute legal advice. Laws and debt thresholds are subject to change. For advice specific to your business's situation, please contact our office to schedule a confidential consultation.

Comments